Ever wondered what happens to the money you keep in the bank? One of the most common and secure ways banks hold your money is through a term deposit. It’s a familiar term you might have heard from family or seen in bank brochures, but what exactly does “term deposit meaning” include?

In this blog, we’ll cover everything about term deposits, what they are, their key features, types, and how they differ from fixed deposits. We’ll also look at how banks use them and the key factors to consider before opening one. By the end, you’ll clearly understand how term deposits work.

So, keep scrolling!

What is a Term Deposit?

A term deposit is a type of bank account where you deposit a certain amount of money for a fixed period, known as the “term”. During this period, the money stays locked, and the bank pays you interest at a fixed rate.

Knowing the term deposit meaning is just the start, let’s explore its key features that define how it works.

Key Features of Term Deposits

Term deposits are known for their simplicity and reliability. Whether you’re setting money aside for a short or longer period, they come with certain features that define how they work.

Guaranteed Interest Rate: The interest rate is fixed when you open the deposit and stays the same throughout, ensuring steady returns.

Set Time Period: You can choose a fixed duration, anywhere from 7 days to 10 years, which remains unchanged once selected.

Withdrawal Rules and Penalties: Early withdrawals are allowed, but banks usually charge a penalty or lower the interest rate.

Stable and Risk-Free: Term deposits are secure and not impacted by market fluctuations. Plus, deposits up to ₹5 lakh (including interest) are insured by the Deposit Insurance and Credit Guarantee Corporation (DICGC).

Customizable Interest Payouts: You can decide how often you want to receive the interest, monthly, quarterly, yearly, or as a lump sum at maturity.

Loan Against Deposit: Many banks offer loans against term deposits, typically allowing you to borrow up to 90% of the deposit amount.

Deposit Amount Limits: Most banks require a minimum deposit of ₹1,000, though this may vary. Generally, there’s no maximum limit on deposits.

Renewal Without Hassle: Banks often provide an auto-renewal feature, renewing the deposit for the same term at the prevailing interest rate upon maturity unless you opt-out.

Knowing the features is important, but did you know term deposits come in different types? Let’s explore them.

Types of Term Deposits

Term deposits come in various forms, each offering unique features to match different financial preferences. Here is a look at the common types of term deposits available in India:

Fixed Term Deposits

You can deposit a lump sum amount for a set period, ranging from 7 days to 10 years. The interest rate is decided upfront and stays the same throughout.

You get the principal and interest together when the deposit matures.

Early withdrawal is allowed, but it usually comes with a penalty.

Recurring Deposits (RD)

Instead of a one-time deposit, you can contribute a fixed amount regularly, usually every month, for a chosen period.

Interest is compounded periodically and paid at maturity, along with the total amount saved.

This type works well if you prefer saving in smaller, consistent amounts.

Senior Citizen Term Deposits

Specially designed for people aged 60 and above, this type offers higher interest rates compared to regular deposits. The tenure options range from 7 days to 10 years, depending on the bank’s policy.

Cumulative Term Deposits

The interest is compounded, usually every quarter or year, and paid out as a lump sum along with the principal at the end of the term. This type is ideal if you’re looking to grow your savings over time without needing regular payouts.

Non-Cumulative Term Deposits

In this type, the interest is paid out at regular intervals, monthly, quarterly, half-yearly, or annually, depending on what you choose. It’s helpful if you prefer to receive periodic income rather than waiting until maturity.

Flexi or Sweep-In Deposits

This type links your savings account to a term deposit.

Any extra money beyond a certain balance automatically moves into the deposit to earn higher interest.

If you need funds, the deposit breaks partially, so you can withdraw without affecting the whole amount.

Post Office Term Deposits

India Post offers these deposits with tenures ranging from 1 to 5 years. Deposits with a 5-year tenure qualify for tax benefits under Section 80C and a minimum deposit of ₹1000.

With the types of term deposits clear, it’s worth exploring how term deposits compare to fixed deposits, a term often used interchangeably but with key differences.

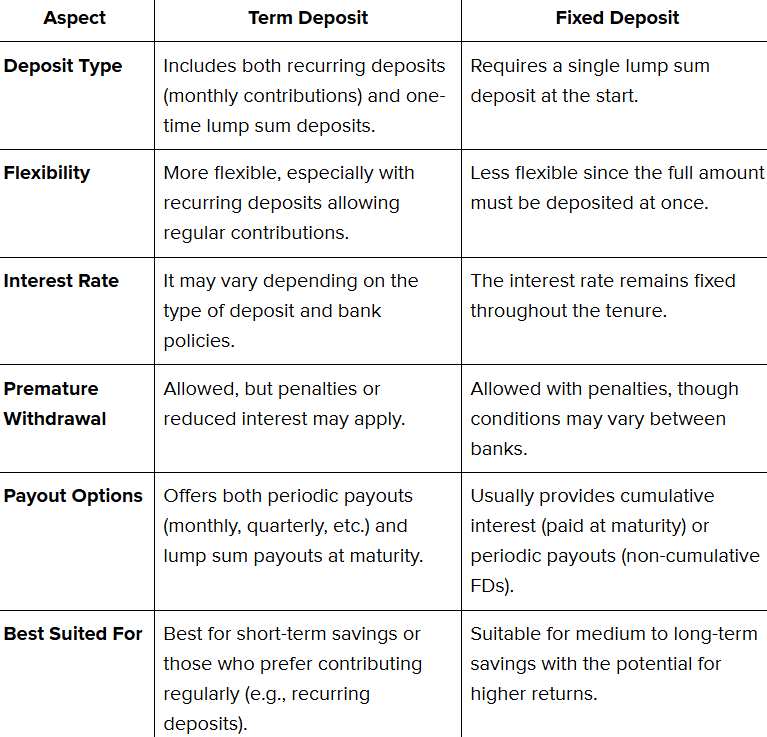

Differences Between Term Deposits and Fixed Deposits

While fixed deposits are a type of term deposit, the two terms aren’t exactly the same. Here are the key differences to help you understand them better:

Knowing the differences is important, but it’s also worth understanding how banks put your term deposit to work.

How Banks Utilize Term Deposits

Banks rely on term deposits as an essential part of their financial operations. This is how banks make use of these deposits:

Providing Loans

Banks use the money from term deposits to offer loans to individuals, businesses, and other sectors. The interest banks charge on these loans is higher than what they pay on deposits, helping them earn revenue.

Ensuring Liquidity

Term deposits give banks a steady flow of funds for a fixed period, helping them manage their cash flow.

Investing in Safe Options

Banks may allocate some of these funds into secure financial instruments like government bonds or other low-risk investments. This helps them earn returns while keeping the money safe.

Meeting Regulatory Requirements

The Reserve Bank of India (RBI) mandates banks to maintain specific reserves, like the Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR). Term deposits form a part of these reserves, ensuring banks stay compliant with regulations.

Launching Special Schemes

Banks often introduce special term deposit plans with competitive interest rates and flexible tenures to attract more customers and gather additional funds. These schemes help banks secure more deposits, especially when loan demand is high.

With a better understanding of how banks use term deposits, it’s time to focus on the factors that matter when choosing the right one for you.

Factors to Consider Before Opening a Term Deposit

Selecting a term deposit isn’t only about where you open it; it’s also about ensuring the terms fit your financial needs. Here are a few key points to consider:

Compare Interest Rates

Interest rates can vary between banks and depend on the tenure you choose. Checking rates across different banks helps you find the most suitable option.

Payout Frequency

Term deposits offer different payout options, monthly, quarterly, annually, or at maturity. Pick one based on whether you need regular income or prefer a lump sum at the end.

Early Withdrawal Policy

If you need money before the tenure ends, check the bank’s penalty charges. Some banks reduce the interest rate, while others charge a percentage of the deposit amount.

Bank’s Credibility

While deposits up to ₹5 lakh are insured by DICGC, it’s still wise to pick a trusted bank with a good track record for reliability and service.

Conclusion

After exploring the term deposit meaning, its features, benefits, types, and key differences from fixed deposits, it’s clear that term deposits remain a secure and structured way to hold your money.

They suit those seeking stability and predictable returns without market-linked risks. Choosing the right type and tenure ensures the deposit aligns with your financial objectives.

For a more balanced approach, diversifying beyond traditional deposits can help enhance your portfolio. Precize, an alternative investment platform in India, offers access to private equity and private credit opportunities with a low minimum investment threshold of ₹10,000, making it easier to diversify.

Reserve your access with Precize today and move toward a more diversified portfolio!

Disclaimer

This blog is for informational purposes only and should not be taken as financial advice. While term deposits are a secure and reliable option, your financial decisions should be based on your individual goals and circumstances. It’s recommended to consult a financial advisor for personalized guidance.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved