Understanding HRA Exemption in the New Tax Regime

Are you aware of how the new tax regime impacts your House Rent Allowance (HRA) exemption? Starting from Assessment Year 2024-25, the Finance Act 2023 has made the new tax regime the default for most taxpayers. While this regime offers simplified tax slabs and higher exemption limits, it removes many deductions and exemptions, including the popular HRA exemption.

This shift has significant consequences for salaried individuals living in rented accommodations. In this blog, we’ll explain the treatment of HRA under the new tax regime, what it means for your taxable income, and how to plan accordingly to manage your tax efficiently.

Understanding these changes helps you make better tax decisions for FY 2024-25 and beyond. Let’s start with a brief overview of what HRA is.

What is House Rent Allowance (HRA)?

House Rent Allowance (HRA) is a key component of many salaried employees’ pay structure, designed to help cover rental expenses.

Key points about HRA include:

HRA is offered by employers as a salary breakup item.

It assists employees in managing housing costs, especially in cities where rents are high.

HRA is usually a fixed percentage of your basic salary and is paid by your employer.

Traditionally, under the old tax regime, a portion of HRA was exempt from income tax, reducing your taxable income and easing your tax burden.

HRA has long been an important tax-saving tool for salaried individuals, but its tax treatment has changed under the new regime. Next, we’ll explore exactly what has changed.

HRA in the New Tax Regime: What Has Changed?

The new tax regime, effective from AY 2024-25, introduces a significant change regarding HRA:

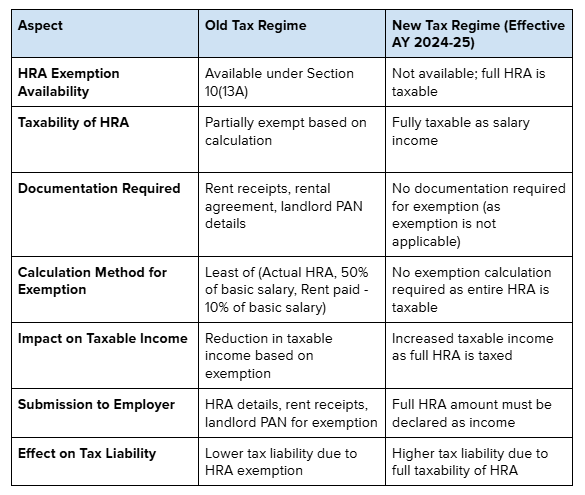

HRA exemption under Section 10(13A) is no longer available.

The entire amount of HRA received by the employee is now fully taxable as salary income.

This means salaried individuals who depend on HRA exemptions will face a higher taxable income, possibly increasing their tax liability.

There is no need to submit rent receipts or landlord PAN for exemption because no exemption applies.

Accurate reporting of full HRA as income is essential for compliance.

It’s important to note that misconceptions about partial exemptions no longer apply (as the entire HRA is now fully taxable under the new tax regime; there is no longer any scope for claiming partial exemptions).

Below is a comparison table highlighting the differences between the old and new tax regimes regarding HRA exemption:

This change requires taxpayers to reassess their tax planning and budgeting under the new regime. Next, let’s see what this means for documentation and employer policies.

Eligibility and Documentation Requirements Related to HRA under the New Tax Regime

While the new tax regime has removed the HRA exemption, there are still important eligibility criteria, documentation, and procedural elements that you need to be aware of:

Eligibility for HRA under the New Tax Regime

Salaried Employees: HRA is applicable only to salaried individuals who receive HRA as part of their salary package. Employees must continue to receive HRA from their employer based on company policies.

Rent Payment: To receive HRA, employees must be living in rented accommodation and paying rent. However, under the new tax regime, HRA is fully taxable, so there’s no exemption to be claimed anymore.

Rent Agreement: While the HRA exemption is not available, employees should have a valid rent agreement in place to establish the rental relationship with the landlord.

Documentation for HRA under the New Tax Regime

Rent Receipts: Rent receipts are no longer required for claiming HRA exemptions but should still be retained as proof of rent payment. These may be needed for employer verification or in case of future tax scrutiny.

Rental Agreements: A rental agreement remains important as it formalizes the rent arrangement between the employee and landlord. While it is no longer needed for exemption claims, it still serves as supporting documentation.

Landlord PAN Details: Landlord PAN details are also not required under the new regime for exemption purposes, but it’s advisable to maintain this information for record-keeping and transparency.

Employer Verification: Some employers may still request rent-related documents for verification or for their own records, even though the HRA exemption is no longer applicable.

Record Keeping

Even though HRA exemption is no longer available, it is important to keep all rent-related documents such as rent receipts, rental agreements, and landlord details for future reference, potential audits, or employer record-keeping. These documents help maintain transparency and ensure compliance with the tax authorities.

Declaration of Full HRA as Taxable Income

Tax Filing: As part of your tax filing under the new regime, you must declare the full amount of HRA received as taxable income. This is crucial for accurate tax reporting and compliance.

Employer’s Form 16: Ensure that Form 16, issued by your employer, correctly reflects the full HRA amount as salary income. This form is necessary when filing your tax returns.

While the removal of the HRA exemption changes the way HRA is treated for tax purposes, understanding the eligibility criteria and documentation requirements is still important for maintaining compliance and transparency in your tax filings.

Next, let’s discuss key points salaried taxpayers should consider under the new tax regime.

Key Considerations for Taxpayers Receiving HRA under the New Tax Regime

With HRA fully taxable, salaried employees need to carefully evaluate their tax and financial planning:

Tax Liability: Expect higher taxable income since no portion of HRA is exempt, potentially increasing your tax bracket.

Budgeting: Plan your rental expenses without the benefit of HRA exemption.

Tax Regime Evaluation: Compare total tax liability between old and new regimes; the old regime might be better if the HRA exemption significantly lowers your tax.

Salary Negotiations: Consider how fully taxable HRA impacts your take-home pay.

Use of Tools: Employ online calculators or consult tax professionals to evaluate options.

Understanding these factors can help you avoid surprises and make informed financial decisions. Now, let’s clarify if HRA exemption calculations still matter.

Is Calculation of HRA Exemption Relevant in the New Tax Regime?

Under the new tax regime, HRA exemption calculations no longer apply because the exemption itself is not available. This means the traditional method of calculating HRA exemption, which involves computing the least of:

Actual HRA received from an employer

50% (metro cities) or 40% (non-metro cities) of basic salary plus dearness allowance

Rent paid minus 10% of the basic salary

— does not apply in the new tax regime.

Instead, taxpayers must declare the full HRA amount as taxable income without any deduction.

How to Declare and Report HRA under the New Tax Regime in Income Tax Returns

When filing your Income Tax Return under the new regime, keep in mind:

Declare the full amount of HRA received as taxable salary income in your ITR.

Ensure your employer’s Form 16 reflects this full amount accurately.

Use certified income tax portals or professional tax-filing software to avoid mistakes.

File your return on time to avoid penalties and notices from the tax department.

Compliance means reporting your full HRA income clearly and correctly.

Final Thoughts

The new tax regime has removed the tax exemption on House Rent Allowance, making the entire HRA component taxable for salaried employees. This change will increase your taxable income and may affect your overall tax planning and budgeting, especially if you live in rented accommodation.

Before finalising your tax strategy, compare the tax implications under both old and new regimes carefully. Use tax calculators or consult with financial advisors to choose the regime that best suits your situation.

For expert assistance in optimising your tax planning and managing your salary components effectively under the new tax regime, explore Precize, which provides tailored financial solutions to help you maximise returns and streamline tax compliance.

Stay informed and plan smartly for a financially sound future.

Frequently Asked Questions (FAQs)

1. What is the impact of the new tax regime on HRA?

The new regime makes the entire HRA amount taxable, removing any exemptions that were available under the old tax regime.

2. Do I still need to submit rent receipts under the new tax regime?

No, rent receipts are no longer required since there is no exemption for HRA under the new regime.

3. How is HRA calculated under the new tax regime?

HRA is fully taxable as salary income, so no exemption calculations apply.

4. Can I still claim HRA if I am living in rented accommodation?

Yes, you can still receive HRA, but it will be fully taxable with no exemption.

5. Should I consider switching to the old tax regime for HRA exemption?

Compare both regimes to see which results in a lower tax liability, as the old regime may still benefit those with substantial HRA exemptions.

Disclaimer

This blog provides general information based on current tax laws and is not a substitute for professional tax advice. Tax regulations may change, and individual circumstances vary. Consult a qualified tax professional or financial advisor for advice tailored to your specific situation before making tax-related decisions.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved