What are fixed-income investments?

What are fixed-income investments?

Fixed-income investments offer guaranteed returns on investments and represent a liability for the issuing organization. These investments generate periodic returns, with interest payments remaining stable despite market fluctuations.

The final value of a fixed-income investment at maturity is determined before issuance and disclosed to the investor at the time of investment. This makes it an attractive option for those seeking secure returns without risk exposure, providing a steady income with additional yields.

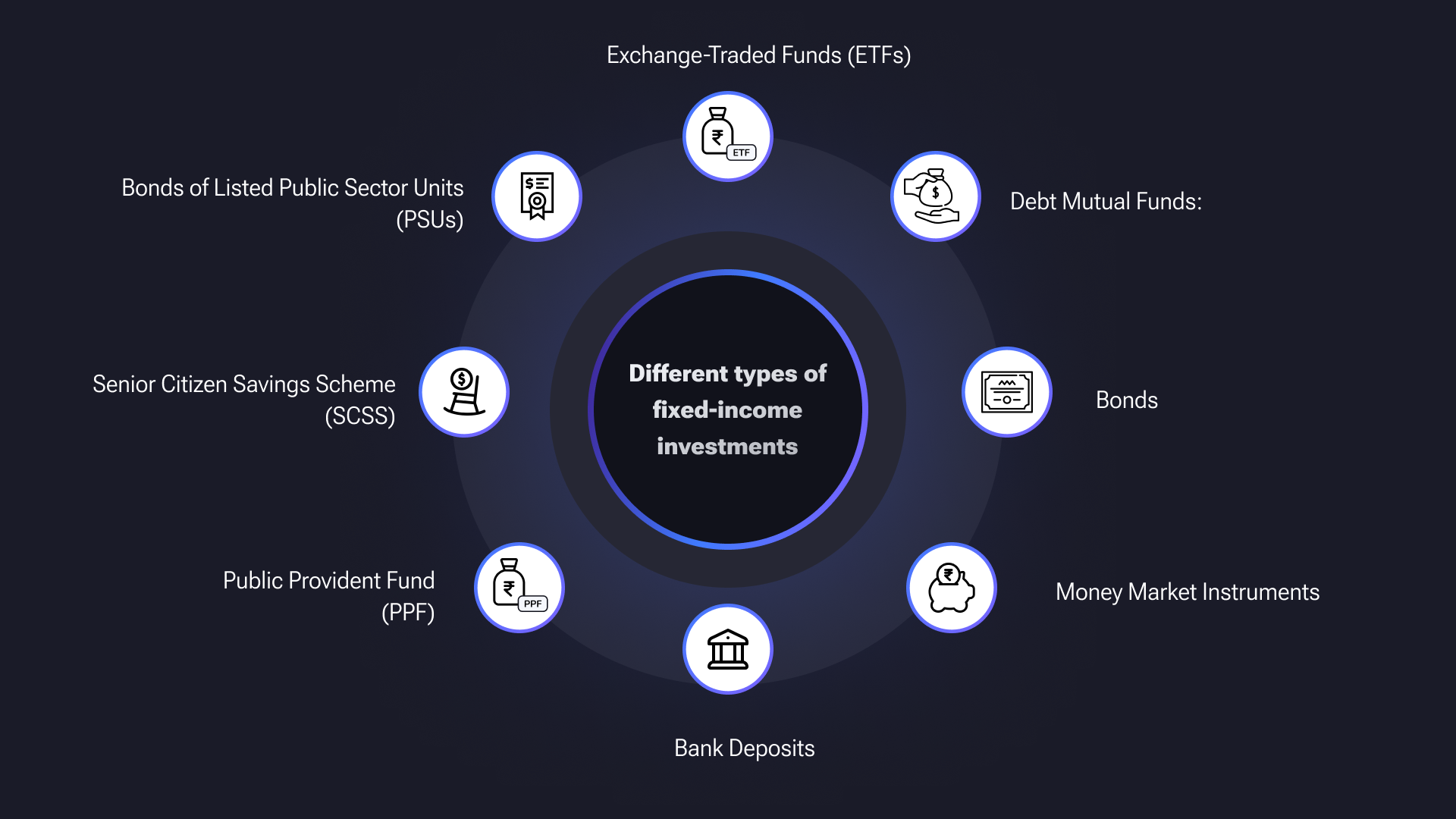

Different types of fixed-income investments:

Exchange-Traded Funds (ETFs): Bond ETFs operate by investing in a variety of debt investments. These investments provide regular and fixed returns and ensure stability with periodic interest payments. These investments are especially favored by retired and risk-averse investors who prioritize stability over potential market gains.

Debt Mutual Funds: These funds pool together capital to invest in various fixed-income investments, such as corporate and government bonds, commercial papers, and money market instruments. The primary advantage of debt mutual funds is that they typically offer higher returns compared to standard savings options like fixed deposits and savings accounts.

Bonds: Bonds are common fixed-income investments issued by companies to finance their daily operations and ensure smooth production. Since bonds act as a liability for the issuer, they must be redeemed once the company generates sufficient revenue.

Money Market Instruments: Treasury bills, certificates of deposit, commercial papers, etc, are money market instruments offered at a fixed rate of interest and are classified under fixed-income investments. These instruments are short-term, typically maturing within a year, and are generally sold over the counter in India, making them accessible primarily through money market mutual funds.

Bank Deposits: Fixed deposits, considered one of the most secure forms of investment, can be held for both short and long tenures based on the investor's preference. However, funds in bank deposits cannot be withdrawn prior the maturity date without incurring a penalty for early withdrawal. There are also various government-sponsored fixed-income bonds:

Public Provident Fund (PPF): Investing in PPF is advantageous due to tax exemptions and higher interest rates compared to regular savings schemes. As a Central Government-sponsored scheme, it carries zero risk.

Senior Citizen Savings Scheme (SCSS): This scheme is designed to provide financial security for senior citizens in India. It offers a substantial interest rate set by the Ministry of Finance. Individuals who are 60 years of age or older are eligible to invest in this scheme.

Bonds of Listed Public Sector Units (PSUs): These bonds are highly popular and attract significant returns as they are issued by top-performing public sector units. They are associated with negligible risk, making them a preferred investment option.

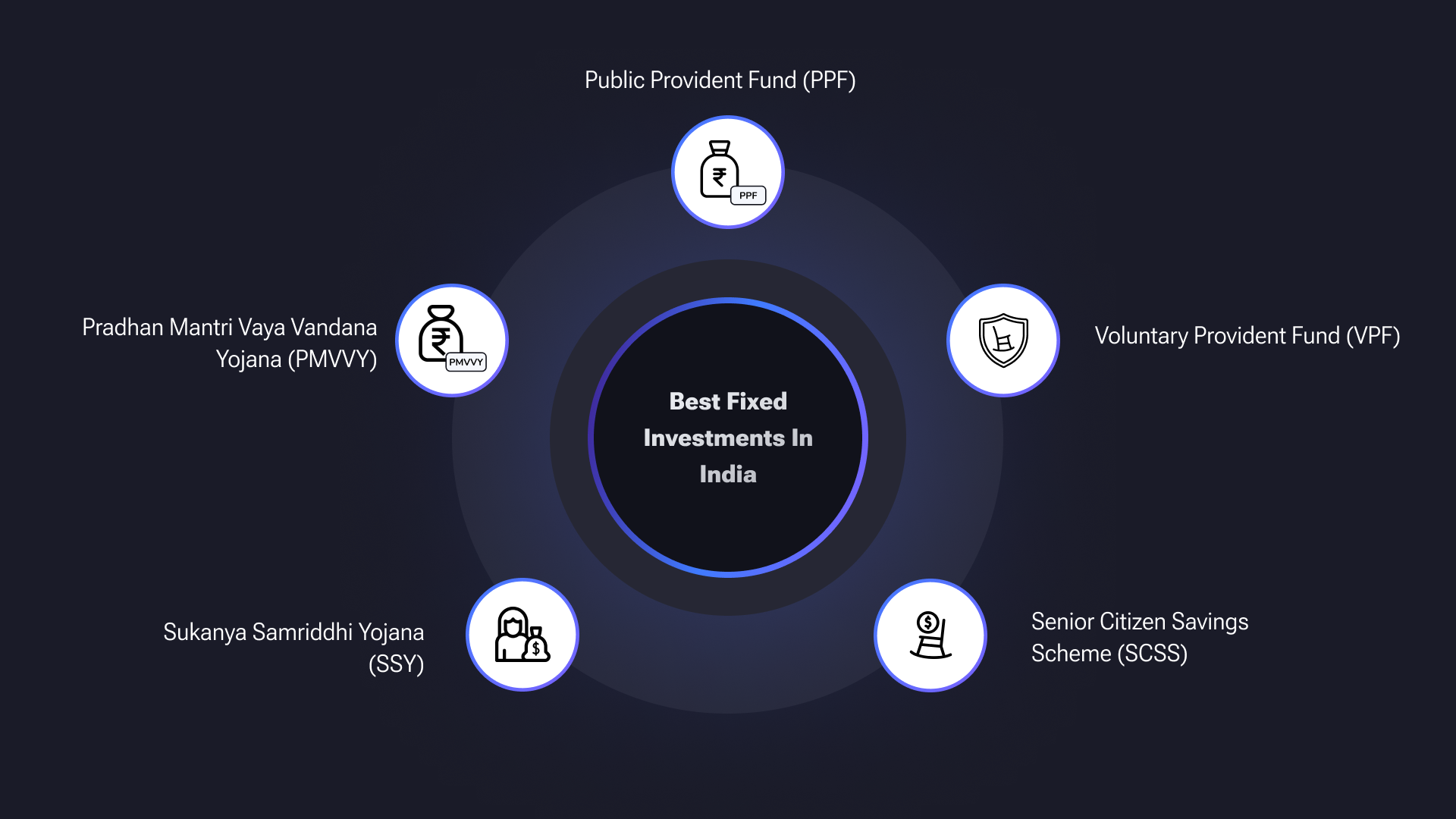

Best Fixed Investments In India:

Public Provident Fund (PPF): Public Provident Fund (PPF) is a long-term investment scheme supported by the Government of India. It offers attractive interest rates that are completely tax-exempt. The initial investment period is 15 years, extendable in blocks of five years. Contributions made to PPF qualify for tax benefits under Section 80C of the Income Tax Act. Investors can contribute a maximum of INR 1.5 lakh annually.

Voluntary Provident Fund (VPF): VPF allows employees to contribute additional amounts to their provident fund account. It's a suitable option for risk-averse investors looking to build long-term wealth.

Listed PSU Bonds: These bonds are issued by government-backed entities with minimal risk of default. Interest income is completely tax-exempt, though capital gains may be taxable.

Senior Citizen Savings Scheme (SCSS): Designed for investors aged 60 and above in a low tax bracket, SCSS provides a regular income stream. The initial investment period is 5 years, extendable by another 3 years, with a maximum investment limit of INR 15 lakh.

Pradhan Mantri Vaya Vandana Yojana (PMVVY): Managed by LIC, PMVVY aims to provide social security to elderly individuals aged 60 and above. The investment limit was recently raised to INR 15 lakh. It offers an assured pension based on a guaranteed annual return of 8% for 10 years.

Sukanya Samriddhi Yojana (SSY): SSY is a small deposit scheme launched under the "Beti Bachao Beti Padhao" campaign for the benefit of the girl child. It offers an interest rate of 8.1% with tax benefits. The scheme can be availed from birth till the girl turns 10, with a minimum deposit of Rs 1000 and a maximum of INR 1.5 lakh annually. The account can remain active for 21 years or until the girl's marriage after turning 18.

Risks Associated with Fixed-Income Investments:

Credit Risk: Debt mutual funds invest in instruments like corporate bonds and treasury bills. Credit risk arises when issuers of these bonds or debt securities fail to repay interest and principal on time. To mitigate credit risk, it's advisable to choose mutual funds that invest in high-quality assets.

Interest Rate Risk: Fluctuations in interest rates directly influence bond prices and, consequently, affect returns from debt mutual funds. When interest rates increase, bond prices generally decrease, and conversely, This is known as interest rate risk.

Considerations before investing:

Before investing in fixed-income bonds in India, there are several important considerations:

Taxation: Capital gains from fixed-income investments are taxable under the Income Tax Act of India, 1961. Long-term gains (holding period more than three years) are taxed at a 20% rate after adjusting for inflation (indexation benefit), while short-term gains (holding period three years or less) are taxed at the investor's applicable income tax rate.

Mutual Funds: Mutual funds that invest in fixed-income bonds are actively managed to maximize returns while ensuring stability. These funds vary in their investment strategies based on their maturity periods. Short-term schemes typically focus on money market instruments and debt funds, while ETFs (Exchange Traded Funds) are suitable for longer investment horizons.

Liquidity: Fixed-income mutual funds are generally highly liquid, allowing investors to redeem their investments easily according to their cash requirements.

These points highlight the key considerations for investors looking to invest in fixed-income bonds in India. Investors should ensure they are aware of taxation implications, investment strategies, and liquidity aspects.

Disclaimer: This information is for private use only and does not constitute investment advice. Recipients must assess risks and seek advice from financial, legal, and tax professionals. Private market investments carry risks, and there are no guarantees of returns or capital protection. We are not liable for investment decisions.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved